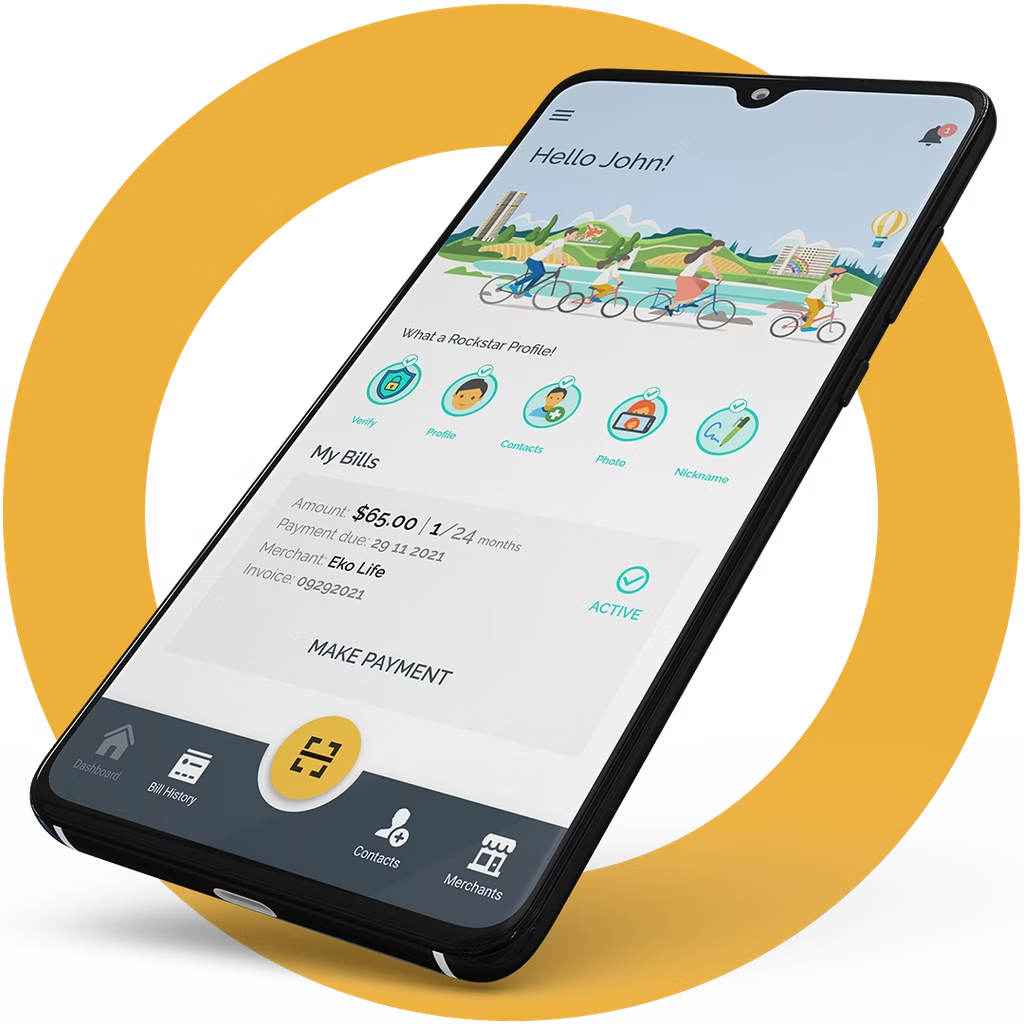

Ready to ride your dream ebike? What are you waiting for…

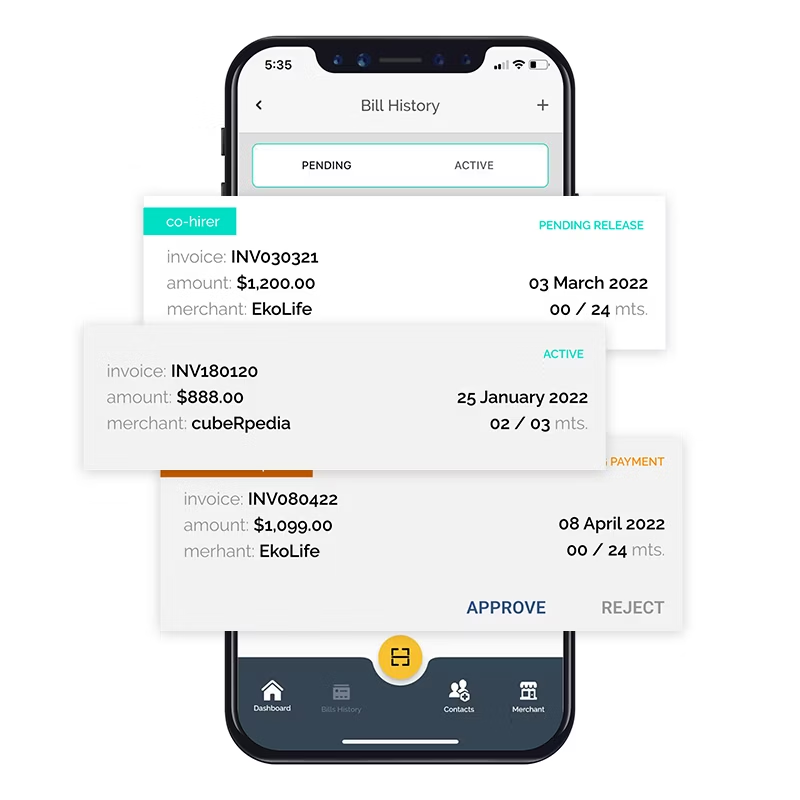

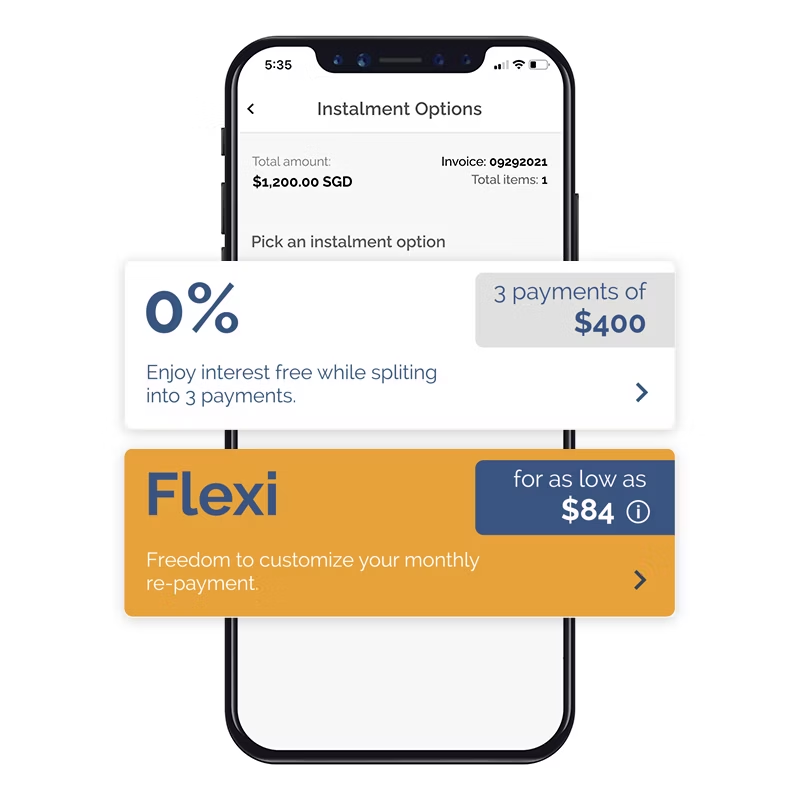

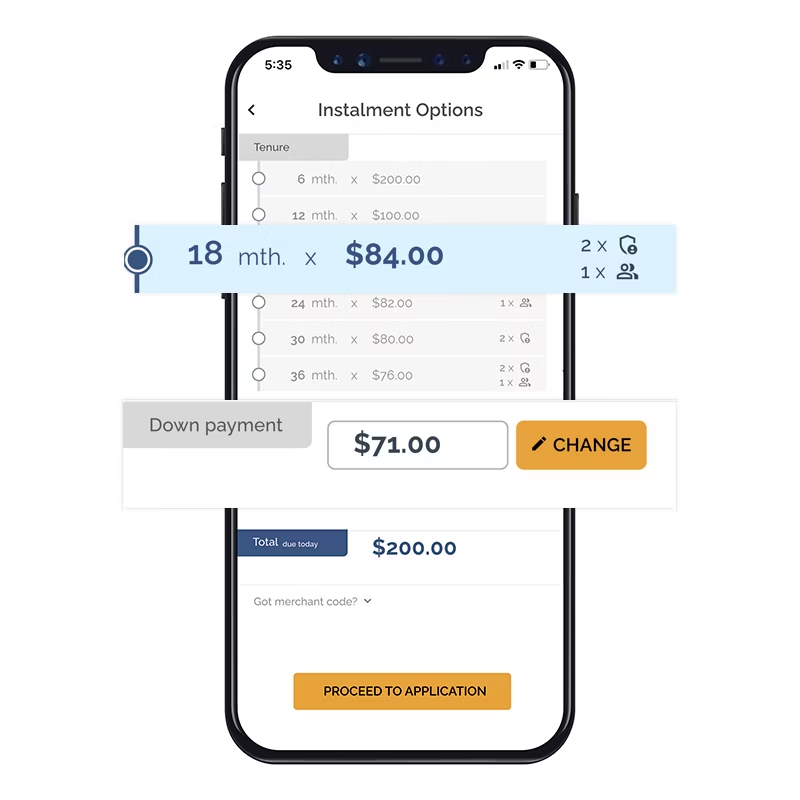

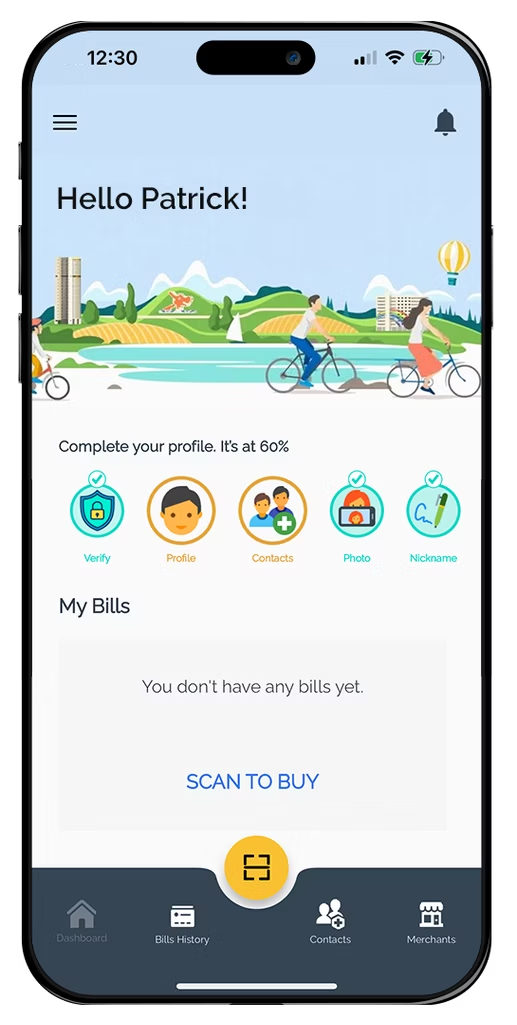

Shop ebikes or bicycles at our merchant partners and pay over time with up to 36-months payment plans. With the Easyride app, say yes to more of the things you love while staying financially responsible.